New studies by Paradigm have shown that Polymarket has been reporting inflated trading volumes.

Research partner Paradigm Storm Slivkoff disclosed that the data on-chain generated by the platform creates a redundant event, and trades are counted twice in nearly all major dashboards.

The research by Paradigm discovered that the principal cause of the discrepancy is that the standard way of adding Polymarket OrderFilled events. Individual lines in each trade register both maker and taker lines, doubling the reported turnover. Slivkoff noted that this has an impact on cash flow and notional volume metrics. As an illustration, a YES/NO token trade of 4.13 will be recorded as $8.26 in the data because of the occurrence being duplicated.

The trade structure of the polymarket generates confusion

The team of Paradigm looked at the structure of trades on Polymarket, where each Polygon transaction is composed of a strict template of one group of orders that are matched. Trades are normally between one taker and one or more makers, placed by approximately 50 externally owned accounts of Polymarket.

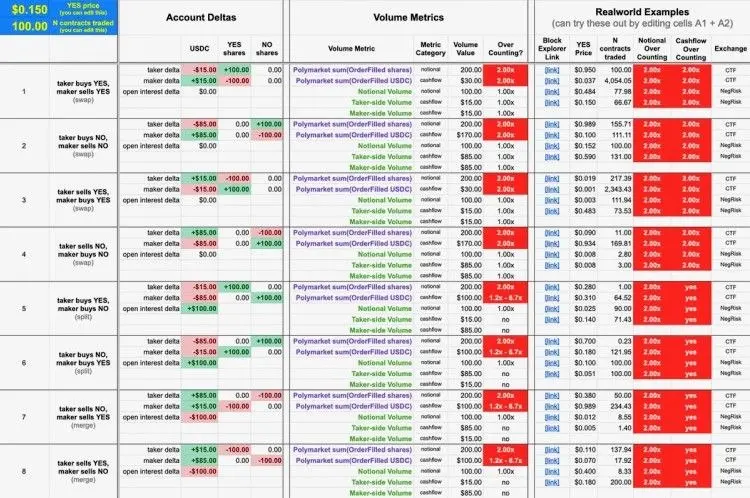

Spreadsheet of the Polymarket volume simulator. Source: Paradigm.

The study pointed out that the Polymarket on-chain data contains complex events, which are misinterpreted by other blockchain explorers. Slivkoff added that this complexity also led to improper accounting practices adopted by analysts, and it is hard to trace the cash flow and open interest. He also added that a type of trade is different in simple swaps, mergers, and splits that would have different impacts on open interest and contract balances.

Simulator shows the correct metrics of volumes

Paradigm created a simulator to simulate at least eight types of trades to shed some more light on trading metrics. The simulator computes changes in maker and taker balance, open interest, and various volumes in relation to two inputs: YES price and the number of contracts traded. Slivkoff proposed that the simulator can be tailored by the analysts to investigate diverse situations.

The study validates that in both cases of the trade, the maker and the taker are in opposing positions where the deltas of both YES and NO contracts are equal in absolute terms. Nevertheless, USDC deltas can vary. The simulator demonstrates that swap trades leave open interest unchanged, whereas split and merge trades raise and lower open interest, respectively. Order-filled event quantities always show double the values of the real amounts of cash flow and notional measures. The exact volumes needed to calculate splits and merges are more complex to calculate.

The results of the work by Paradigm show that there is a systemic accounting problem on Polymarket, where the counts of trades are being reported twice across dashboards. The standard data providers (analysts) can overestimate activity. The simulator offered by Paradigm offers a more accurate method of testing the trading volumes and provides a better perception of the market dynamics of the platform.